Having a Backup Plan

As people work longer, they often carry major financial responsibilities, such as mortgages and college loans, into their later years.1–3 Someone who has high medical expenses or a spouse who no longer works may have to shoulder a heavier load than a younger person.

If you’re still working, have you considered what might happen if you were suddenly unable to earn a paycheck as the result of an illness or injury? Would you have to dip into your retirement savings to pay bills? Could you afford your medical expenses if you lost your income?

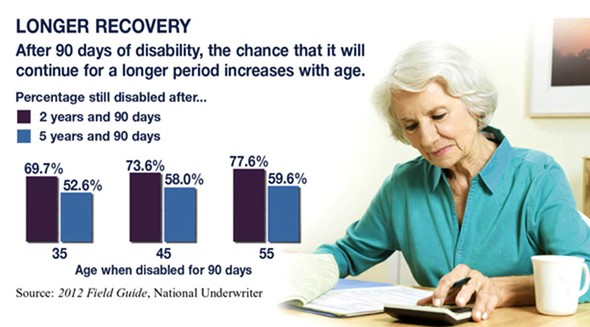

Although most people would prefer not to think about the possibility of being disabled, the odds might surprise you. A 50-year-old has a 36% chance of experiencing at least one long-term disability (lasting 90 days or more) before age 65.4 Nine out of 10 disabilities are caused by common illnesses and health conditions such as back problems rather than by injuries.5

Replacing Your Income

If an illness or injury resulted in your being unable to work, an individual disability income insurance policy could help replace a percentage of your income, up to the policy limits. Benefits may be paid for a specified number of years or until you reach retirement age. Some policies pay benefits if you cannot work in your current occupation; others might pay only if you cannot work in any type of job. If you pay the premiums yourself with after-tax dollars, benefits are usually free of income tax.

Your employer may offer long-term disability coverage, but group plans typically don’t replace as large a percentage of income as an individual plan could. Benefits from employer-paid plans are taxable to the employee if the employer paid the premiums. Of course, if you change jobs, you might lose your subsidized employer-based coverage.

A loss of income could alter your options for retirement. An appropriate individual disability insurance policy may help protect you and your family during a difficult time.

1) U.S. Bureau of Labor Statistics, 2012

2) AARP, 2011

3) Chicago Tribune, July 12, 2012

4) 2012 Field Guide, National Underwriter

5) CNNMoney, June 26, 2012

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright © 2013 Emerald Connect, Inc.