Understanding High-Deductible Medical Plans

In 2012, total health-care costs for an American family of four covered by an employer-sponsored PPO insurance plan averaged $20,728. Employers contributed $12,144 of the total and employees were responsible for $8,584 (through payroll deductions and out-of-pocket expenditures).1

Rising health-care costs are the main reason that more Americans are finding medical plans with higher deductibles in their workplace benefit offerings. A deductible is the amount the insured must pay before insurance payments kick in.

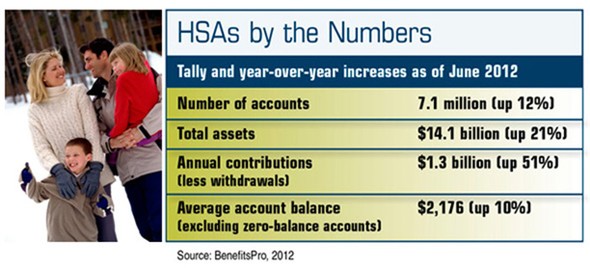

High-deductible plans may be supplemented with health savings accounts (HSAs), which are funded with pre-tax dollars. HSA funds can be used to help pay insurance deductibles and out-of-pocket medical costs. To be eligible for an HSA in 2013, individuals must be enrolled in medical plans with deductibles of at least $1,250 ($2,500 for families).2

The percentage of workers enrolled in high-deductible plans has more than quadrupled from 4% in 2006 to 17% in 2011. Seventy percent of large companies surveyed plan to offer high-deductible insurance in 2013, and nearly 20% of respondents said it would be the only option for employees.3

What was once considered “catastrophic” coverage could soon become the norm. For many workers (and self-employed individuals who purchase their own policies), a high-deductible plan, managed in combination with an HSA, may be a more affordable and flexible health insurance option.

The Difference Is in the Details

Premiums are typically lower for high-deductible plans than they would be for traditional HMO and PPO health plans. With an HSA-qualified plan, however, members usually pay more up-front for services such as physician visits, surgical treatments, and prescriptions (but typically receive the insurer’s negotiated discounts). Annual physicals, health screenings, and some other types of preventive care are often provided at no cost.

Policies typically have out-of-pocket maximums, above which the insurer pays all costs. In 2013, the upper limit is $6,250 ($12,500 per family), but plans may have lower caps. This feature can help policyholders budget accordingly for a “worst case” scenario.4

HSA Rules

Workers decide how much money to divert to their HSAs using pre-tax payroll deductions, up to the annual maximum contribution limit ($3,250 for individuals or $6,450 for families in 2013).5 An additional $1,000 can be contributed starting the year in which a participant turns 55.6 In lieu of higher premiums, some employers make an annual contribution to employees’ HSAs.

Unlike the case with more restrictive flexible spending accounts (FSAs), participants do not lose unused health savings account funds at the end of the year. Unspent HSA balances can be invested and used to help meet medical needs in future years. HSA funds belong to the workers, who can keep their accumulated assets even if they change employers or retire. Later, in retirement, HSA funds could be used to help pay for Medicare premiums or long-term-care expenses.

HSA funds can be withdrawn free of federal income tax and penalties provided the money is spent on qualified health-care expenses. Depending on the state, HSA contributions and earnings may or may not be subject to state taxes.

High-deductible plans are designed to help restrain medical spending by offering people the financial incentive to focus on wellness, change unhealthy habits, and become more informed health-care consumers. Generally speaking, families that are willing to compare pricing for medical providers, stay in their plan’s network for tests and services, buy generic prescription drugs, and take other proactive steps to limit their out-of-pocket health expenses may be more likely to benefit from high-deductible insurance.

1) Milliman, 2012

2, 4–5) BenefitsPro, 2012

3) Kaiser Family Foundation, 2012

6) usnews.com, June 5, 2012

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright © 2013 Emerald Connect, Inc.